Wall Street’s Wednesday Shutdown: From $4B Paper Crisis to $5.5T Tokenized Finance

On June 12, 1968, the NYSE made an unprecedented decision: close every Wednesday. Not because of war, not because of a market crash—but because of too much paper. Daily trading volume had surged from 10 million to 21 million shares, burying back offices in physical stock certificates. SEC Commissioner Ray Garrett Jr. later recalled: “Everybody agreed that the securities-processing system had virtually broken down.” Over $4 billion in trades remained unprocessed, and more than 100 broker-dealers failed.11

This crisis birthed an institution called DTC—the Depository Trust Company, founded in 1973 with a simple mission: stop moving securities with paper. DTC did something radical for its time: it locked all physical certificates in a central vault and handled trades through electronic book-entry transfers. This was the beginning of the dematerialization revolution.

What Dematerialization Changed

After dematerialization, Wall Street was transformed. Settlement cycles gradually shortened from T+5 during the paper crisis to T+3 (1993), T+2 (2017), and finally T+1 in May 2024—a reduction of four-fifths. Trading volume exploded: the 21 million daily shares that broke the system in 1968 first surpassed 100 million in 1982, and today’s U.S. equity market routinely processes over 10 billion shares per day. Without DTC and its successor DTCC, this scale would be impossible.12

DTCC, born from the paperwork crisis, has become the central plumbing of the global financial system: custodying over $114 trillion in assets, processing approximately $4.7 quadrillion in securities transactions in 2025, covering virtually all U.S. equities, corporate bonds, municipal bonds, and money market instruments. Over 1.44 million securities issues from 170+ countries flow through its systems daily. From “cannot handle paper” to “processing the world’s securities,” DTCC completed a total infrastructure upgrade in fifty years.13

Fifty Years Later, the Same River

On May 4, 2026, DTCC—the institution born from the paper crisis—announced a far more radical plan: tokenizing $114 trillion in custodied assets onto the blockchain. This is not a crypto startup’s whitepaper. This is the core plumbing of the global financial system speaking. From paper crisis to dematerialization, from dematerialization to tokenization—the historical rhyme is striking: each time, when old infrastructure could no longer carry new transaction volumes, the next generation of infrastructure emerged.14

Signal One: The $114 Trillion On-Chain Plan

The SEC granted a three-year No-Action Letter on December 11, 2025, authorizing DTCC to tokenize Russell 1000 constituents, ETFs, and U.S. Treasuries. Limited production trades begin in July 2026, with a full service launch in October. Over 50 institutions have joined the Industry Working Group—BlackRock, Goldman Sachs, JPMorgan, Nasdaq, BNP Paribas, Citi, Morgan Stanley, plus crypto-native firms like Circle and Anchorage Digital.15

This is not about building a parallel market on blockchain. DTCC’s tokenized assets will remain within the DTC custody system, carrying the same ownership rights, investor protections, and legal standing as traditional securities. What changes is not the asset itself, but its digital representation. As Nadine Chakar, DTCC’s Global Head of Digital Assets, stated: “Tokenization is an important and critical step toward building tomorrow’s digital infrastructure.”16

Signal Two: Citi’s $5.5 Trillion Forecast

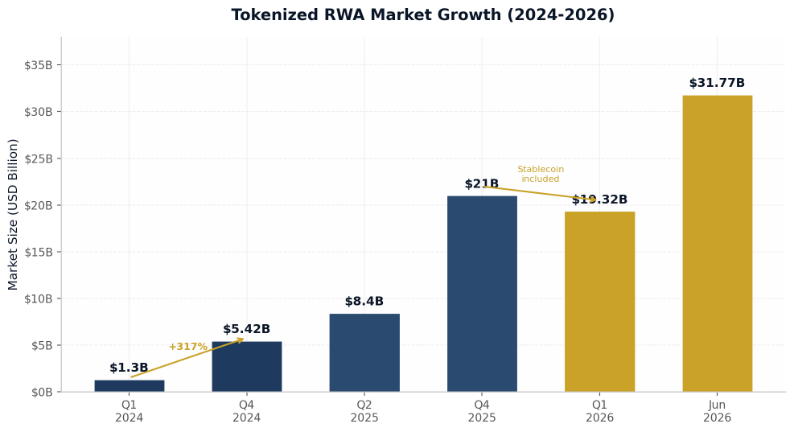

On June 1, 2026, Citi released its “Tokenization 2030: Wall Street On-Chain” report ahead of the Proof of Talk conference in Paris. Citi projects the tokenized securities market will reach $5.5 trillion by 2030 (base case), with a high scenario of $8.2 trillion. The forecast assumes 10% of U.S. Treasury bills and 3% of U.S. listed equities will be tokenized, with stablecoin float reaching $1.9 trillion.17

Figure 1: Tokenized RWA Market Growth (2024-2026) Source: CoinGecko, RWA.xyz

BlackRock’s BUIDL fund has surpassed $2.5 billion in AUM, Franklin Templeton’s BENJI exceeds $1 billion, and Ondo Finance’s tokenized treasury products OUSG and USDY collectively manage approximately $2.6 billion. Traditional asset managers are voting with real capital—this is not speculation, but a bet on market structure evolution.18

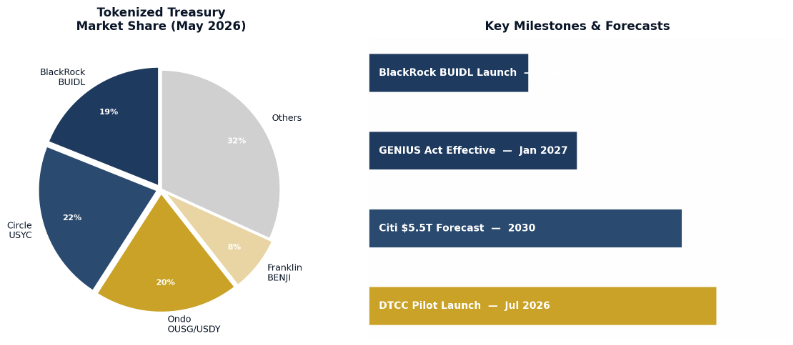

Figure 2: Tokenized Treasury Market Share & Key Milestones Source: rwa.xyz, Citi Research

Signal Three: GENIUS Act and the Regulatory Green Light

The GENIUS Act, signed in July 2025, is the first comprehensive U.S. federal stablecoin legislation. It mandates 1:1 reserves in high-quality liquid assets and subjects issuers to federal oversight by the OCC, FDIC, and FinCEN. Proposed rules were published between February and April 2026, with final regulations expected by July 2026 and full effectiveness by January 18, 2027.19

This regulatory clarity is becoming the “passport” for institutional capital. Meanwhile, competition is heating up: Nasdaq is partnering with Payward (Kraken’s parent) to develop a blockchain stock trading system targeting a 2027 launch; ICE (NYSE’s parent) has partnered with crypto platform OKX. The tokenized securities race has shifted from “whether” to “who gets there first.”20

Conclusion: Asset On-Chain Is Irreversible, On-Ramp Defines the Winners

From the $4 billion Paper Crisis of 1968 to the $5.5 trillion tokenized finance vision of 2026, three independent signals point to one conclusion: asset on-chain is irreversible.

Why irreversible? Because history has already given us the exact same script. After the paper crisis, settlement shortened from T+5 to T+1, trading volume exploded from 21 million to 10+ billion shares daily, and paper certificates gave way to electronic book-entry—all driven not by any single institution’s radical experiment, but by the natural evolution of the financial system under efficiency pressure. Today’s tokenized finance is replaying the same logic: the GENIUS Act provides federal regulatory certainty, DTCC has placed $114 trillion of assets on the tokenization roadmap, and traditional giants like Citi, BlackRock, and Goldman Sachs are betting real capital—this is not a fringe experiment, but a systematic upgrade of market infrastructure.

Why, then, is the next phase of competition not about “which assets can be tokenized” but about “who can build the on-ramp that institutions trust, regulators understand, and markets accept”? The answer lies in DTCC’s own history. Recall: DTCC’s fundamental problem was never “can people buy stocks”—people could always buy stocks. DTCC solved “after buying, how do you deliver, settle, and ensure safety.” Tokenized finance today faces the exact same proposition: asset on-chain is only step one; the real infrastructure challenge lies in compliance, custody, settlement, trading, investor protection, and cross-border regulatory mapping.

Why do the convergence of RWA, compliant exchanges, and stablecoin settlement matter? Because for tokenized finance to become institutional-grade infrastructure, it must simultaneously solve three problems: the asset side (what assets can go on-chain), the funding side (what to settle with), and the compliance side (who regulates, how). RWA solves the asset side—BlackRock’s BUIDL and Franklin Templeton’s BENJI have proven institutional-grade asset tokenization is viable; compliant exchanges solve the intersection of funding and compliance—Nasdaq and ICE are integrating tokenized securities into existing trading frameworks; stablecoin settlement solves on-chain cash—the GENIUS Act means stablecoins are entering federal regulatory tracks, becoming the preferred settlement tool for tokenized assets. All three are indispensable, and their intersection is the core on-ramp for next-generation financial infrastructure.

Who are the leaders at this on-ramp? Three dimensions of early movers are already taking shape: On the asset side, BlackRock leads with BUIDL’s $2.5+ billion AUM, followed by Ondo Finance at ~$2.6 billion; on the infrastructure side, DTCC’s $114 trillion custody scale is unassailable, while Citi, JPMorgan, and Goldman Sachs are building institutional service frameworks; on the trading and settlement side, Circle’s USYC (tokenized cash instrument) and Nasdaq’s blockchain stock system represent two different paths. In the Asia-Pacific region, Hong Kong’s dual strength as a traditional financial center and digital asset regulatory pioneer positions it as a key gateway for institutional access to tokenized finance. Platforms like EXIO, with both compliance DNA and technical capability, stand at this historic crossroads—the next fifty years of finance will be defined by today’s on-ramp builders.

About EXIO Group

EXIO Group is a leading global digital asset fintech group dedicated to building innovative infrastructure connecting traditional finance and the digital economy. The Group implements a multi-dimensional compliance strategy, strictly adhering to local regulatory frameworks in major financial centers worldwide. Our core platform integrates seamless fiat-to-digital asset conversion, institutional-grade asset custody, Real-World Asset Tokenization (RWA), and cutting-edge PayFi (Pay-to-Finance) solutions. Leveraging strategic partnerships with leading international banks and a top-tier team comprised of traditional financial elites and blockchain technology experts, EXIO continues to lead industry innovation, providing secure, compliant, and forward-looking digital asset financial services to institutional clients globally.

Disclaimer:

This material is for general information and research purposes only and does not constitute any investment, financial, legal, or tax advice, nor does it constitute any solicitation, offer, or recommendation. The content may contain third-party information or opinions, which do not represent the official position of any institution or individual. Prices of virtual assets and related products may be highly volatile. Investors should make independent judgments based on their own financial situation, investment objectives and risk tolerance, and conduct their own research (DYOR) and consult independent professional advisors before making any investment decisions. No party shall be liable for any loss arising from the use of or reliance on this material, except as excluded or limited by applicable law.

References

[1] TradingHours.com, “NYSE Historical Trading Schedules.” Paperwork Crisis closure: June 12 – December 31, 1968.

[2] SEC Commissioner Ray Garrett Jr., testimony before Congress, 1974.

[3] Headcount Coffee, “1968 Paperwork Crisis Forced NYSE Trading Halt,” February 2026.

[4] Crestwood Advisors, “The Evolution of Trade Settlement,” April 2025. Settlement cycle: T+2(1952)→T+5(1968)→T+3(1993)→T+2(2017)→T+1(2024).

[5] DTCC 50th Anniversary, dtcc.com, May 2023. “DTCC has been shaping and advancing the financial services industry since DTC was created in 1973.”

[6] DTCC Annual Report 2025. DTC custodies over $114 trillion; processed $4.7 quadrillion in securities transactions; 1.44 million securities issues from 170+ countries.

[7] NYSE Historical Trading Volume. 1982: first 100M daily shares; current: 10B+ daily shares.

[8] Britannica Money, “T+1 Settlement Meaning, Timeline & Impact.”

[9] DTCC, “DTC Tokenization Service Industry Working Group Update,” May 4, 2026.

[10] SEC No-Action Letter to DTC, December 11, 2025 (three-year authorization).

[11] Tradeweb, “DTCC Advances Development of New Tokenization Service,” May 4, 2026. 50+ firms including BlackRock, Goldman Sachs, JPMorgan, Circle, Anchorage Digital.

[12] CryptoNinjas, “DTCC Targets $114T Tokenization Push With 50+ Firms,” May 5, 2026.

[13] Blockhead, “DTCC Sets July Pilot, October Launch for Tokenized Securities,” May 5, 2026.

[14] Nadine Chakar (DTCC), quoted in Blockhead coverage, May 2026.

[15] Citi GPS, “Tokenization 2030: Wall Street On-Chain,” June 1, 2026. Ronit Ghose, Citi Global Head of Future of Finance.

[16] CoinGecko, RWA Market Data, Q1 2026. RWA market grew 256.7% YoY to $19.32B (non-stablecoin).

[17] rwa.xyz, Tokenized Treasury Tracker, May 2026.

[18] GENIUS Act, Pub. L. No. 119-XXX, signed July 2025; effective January 18, 2027.

[19] OCC Proposed Rule on Stablecoin Supervision, Federal Register, February 2026.

[20] FDIC Proposed Rule on Stablecoin Reserve Requirements, March 2026.

[21] FinCEN Proposed Rule on Stablecoin AML/CFT Compliance, April 2026.

[22] Nasdaq blockchain stock system with Payward (Kraken parent), targeting 2027 launch. DTCC coverage, May 2026.

[23] ICE (NYSE parent) partnership with OKX. Blockhead coverage, 2026.

[24] AInvest, “DTCC’s July 2026 Tokenization Launch: A Flow Test for Traditional Finance,” May 2026.

[25] Frank La Salla (DTCC President & CEO), quoted in DTCC announcement (May 4, 2026) and PYMNTS coverage.